Authors: Nora Hiller (IEEP), Ed Worsdell and Clara Vullo (IEEP UK)

The UK’s proposed Forest Risk Commodity (FRC) regulation and the EU’s Regulation on Deforestation-free Products (EUDR) are frameworks for tackling global deforestation. With the UK’s regulation still under development, and the EUDR subject to repeated delays and simplification, the chance remains for alignment – or for divergence. This insight piece takes stock of the ongoing political developments on both sides of the channel, giving an outlook on the challenging times ahead.

EU developments

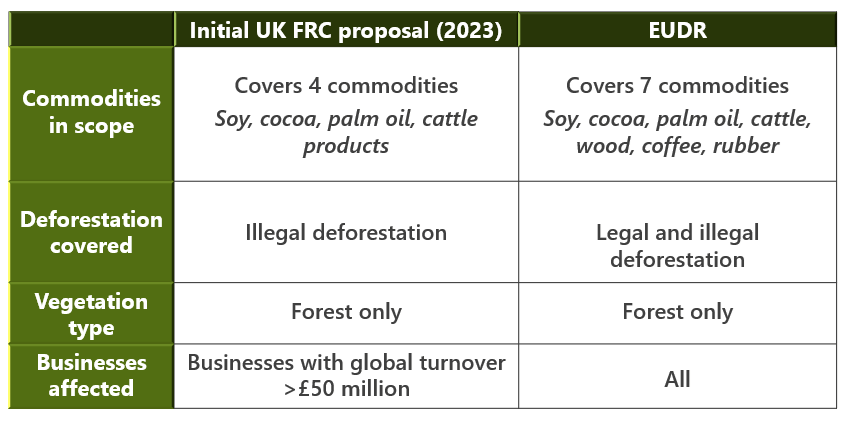

This January would have been the start of the EUDR in action, aiming to prevent deforestation and forest loss from conversion to agriculture. In comparison to the proposed UK regulation, it covers a wider range of commodities and prohibits both legal and illegal deforestation (see table below). In December 2024, following tense political discussions on industry readiness, EU co-legislators decided to delay the EUDR. Similar events unfolded in 2025 over IT issues. During that process, more far-reaching changes in the text of the Regulation were made by the EU institutions, in line with the European Commission’s simplification agenda and competitiveness drive. These changes have produced an amended, weakened Regulation which may affect both the effectiveness and enforcement of the regulation and EU-UK cooperation on halting global deforestation.

One aspect of this simplification is the erosion of supply chain transparency. While the EUDR foresaw companies providing supply chain transparency from the plot to the consumer, the responsibility to provide a due diligence statement is now reduced to the first point of entry into the EU market. Small and medium enterprises in low-risk countries, including the UK, are required to provide a one-time declaration. As a result, accountability to provide information is not distributed across the supply chain, weakening the overall transparency and the system’s capacity to detect risks and inconsistencies. The revision also removed printed products from the scope, without a publicly available assessment. More modifications lie ahead before the EUDR is implemented, with a simplification review focused on the impact and administrative burden mandated for April 2026.

An unpredictable regulatory environment may damage the EU’s international reputation, its credibility towards trading partners, and the companies and governments that have already invested heavily in compliance. With this in mind, is the EUDR still a flagship model for the UK?

UK developments

Action to tackle deforestation in UK commodity supply chains is critical – in 2024, only 0.3% of cocoa and 4.5% of soy products in UK retailers were verifiably deforestation-free. In a bid to begin to address this issue, the UK’s 2021 Environment Act introduced new requirements for UK businesses banning the use and sale of forest risk commodities and derivatives in the UK that have been produced in a manner that does not comply with local land use laws. This framework will require secondary legislation to determine its scope, due diligence requirements and implementation timeline. An initial scope proposed in 2023 by the previous Conservative Government was notably narrower than the EUDR, both in terms of products covered and its focus on only illegal deforestation. Comparisons to those aspects of the EUDR that have been watered down in recent simplifications are harder to make, given that the UK proposal was light on detail in these areas.

The current Labour Government has previously confirmed, both in its election manifesto and in post-election communications, its support for the introduction of UK FRC regulations. However, four years after the passing of the Environment Act, the secondary legislation required to determine this regime’s scope, due diligence reporting requirements and implementation timeline has yet to be tabled.

In early 2025, Minister for Nature Mary Creagh, under whose portfolio the FRC regulations fall, reasserted the Government’s support towards global efforts to protect forests, without committing to an implementation date. This “in due course” approach was reiterated at the end of April during a Westminster Hall Debate dedicated to policies to limit global deforestation, and in response to a written question in November 2025. It is becoming increasingly apparent that the UK Government is monitoring developments in the EUDR before making a final decision on how these rules will be implemented in the UK.

What does this mean for UK-EU cooperation in this area?

A webinar organised by IEEP UK in October 2025 addressed possible alignment or divergence between UK FRC and the EUDR. Pippa Heylings MP underlined the urgency of robust legislation to protect biodiversity and indigenous communities, warning that loopholes risk making the UK a backdoor for commodities not meeting EU standards. Nicola Brennan (WWF-UK) and Joe James (Sainsbury’s) discussed the retailers’ responsibility, noting the limits of voluntary action and the benefits of regulatory alignment. The conversation also outlined the impact of deforestation in areas such as the Cerrado and Pantanal, areas of other wooded land and wetlands. The European Commission was initially set to consider these biodiverse ecosystems for the EUDR in a 2024/25 review, now moved to a general review in 2030. These areas do not currently fall under the provisional scope of UK FRC regulations.

Whilst there has been no seeming desire in the UK to slash ‘green tape’ to gain a competitive advantage over its EU neighbours, neither has there been an objective

At a time when 8.1 million hectares of biodiverse forest are lost annually, and worldwide private sector commitments – such as the Amazon Soy Moratorium – are being eroded, the application of robust measures through the EUDR and UK FRC regulations becomes even more important. In light of Europe’s history of exploitation, it carries a global responsibility to prevent further fuelling of deforestation through its consumption of forest-risk commodities.

Given the recent simplifications, the first step would be to see legislation in place and implemented in both the UK and EU. Since the EUDR is further developed, and building on the recent mood from the UK Government to align with EU standards to remove trade barriers, there is a strong case for the UK aligning with the EUDR to secure close EU-UK cooperation and create a complementary or even harmonised system. Without alignment, companies operating across these markets can expect to operate in unique systems with inefficiencies – including increased compliance costs – and with greater exposure to liability for inadequate due diligence in either the UK or the EU. Regulatory alignment early on would, on the contrary, favour common approaches to address implementation challenges and make it easier for businesses to navigate the system. It would also favour common thinking on the extension of the respective regulations to other ecosystems (such as other wooded land, wetlands or peatlands) and new commodities (such as meat other than cattle), thus eventually incrementally improving their impact for both partners.

Given the recent simplification of the EUDR however, another option that has been suggested is for the UK to aim higher than the EUDR to mitigate its shortcomings and drive a ‘race to the top’ in environmental standards. This would, however, require a strong case around the environmental benefits set against the business/trade impacts of operating two parallel systems. With the UK having previously outlined a different approach to the EU, however, this argument holds less weight.

Photo by Matt Palmer on Unsplash